This month has been relatively bad for Malaysia. The Ringgit has dropped in strength in relation to the greenback (US Dollar) and the FBMKLCI has dropped more than 6.5% Year To Date (YTD).

[FBMKLCI : capitalisation-weighted stock market index made up of Malaysia's big 30 companies]

The implications:

1) For ringgit holders expect a higher expense when dealing in dollars. And due to the high currency fluctuations worldwide (the ruble/yen etc), the impact is limited to your dealings, in your transacted currency.

2) Malaysian stock market still presents bargains, ever more now that valuations are getting cheaper

According to Peter Lynch, if one could predict interest rates (or macroeconomic conditions for that matter) there would be many billionaires out there which is numerically impossible.

[Peter Lynch is an American businessman and stock investor. As part of his role at Fidelity Investments, he managed the Magellan Fund between 1977 and 1990 averaging a 29% return, making it the best 20-year return of any mutual fund over the period. Wikipedia]

In other words, there are bargains out there currently but no one knows or will know how low prices may go. For instance, one would regard these stocks as cheap; Oldtown, small-medium housing stocks i.e. Titijaya, GAB and others.

Oil stocks are definitely down i.e. Petronas Dagangan bhd, SapuraKencana Petroleum Bhd, Barakah Offshore Petroleum Bhd and due to our institutional inspectors fondness of the sector, I would regard the cheapness an opportunity. HOWEVER, one should consider evaluating historical performance of oil companies in low oil prices environment. A look back at companies when oil tanked in price would be a good start.

Only after considering essential points and the sector's fundamentals i.e. nature of an oil company (upstream or downstream/new or old oil fields available/cost of production/long term fixed or variable contract etc) then investing is recommended.

In deciding to invest more in Malaysian stocks, consider watching this great find, a video explaining a simple approach to investment by Mr Lynch (whom also reminds one of Philip A Fisher's theories and principles i.e. the scuttlebutt approach).

Making Money in the Stock Market:

Peter Lynch on Investing in the U.S. Economy (1994)

http://youtu.be/Lxypq_qIw7M

In brief, his ideology is similar to Warren Buffett's principle of : you only need to make 20 good investment decisions in 1 lifetime from his famous line that basically states;

“Your financial wealth would be much greater if you could only make 20 investments in your lifetime. You would make sure they were great if you had only 20 chances.”

Happy investing.

Tuesday, 30 December 2014

Wednesday, 22 October 2014

Global Economy September 2014

It is earning season in the States (US). The Dow Jones (not particularly liked; being a market-total price-weighted index) will see fluctuations that will fluctuate global stock markets.

US markets recently had a "10% correction" which should happen 1x annually (prior US gov intervention). This correction has occurred twice this year; in February and October. Can these corrections suffice for a 20% correction?

[relevant 10% correction article: http://www.cnbc.com/id/102106829]

Mr Buffett would rightly say always buy undervalued companies. In case of a further 20% correction (that used to occur every 3.5yrs that is long due now), your unrealised losses should your stock price accord the market, be minimal.

Hence, the answer would be maybe yes, maybe no.

Notice that all mega investors as such Mr Buffet, mr Li Ka Shing, Mr Al-Waleed bin Talal have all invested in undervalued companies successfully with a key ingredient. Cash.

During the roughest of times, they have all invested what cash they had accumulated into now cheap, quality stocks and companies.

In other words, they invest in cheap/undervalued companies all year round while keeping a good amount of cash in case of any market correction.

This is also the strategy of Tan Teng Boo the captain of Capital Dynamics, a closed end fund with about RM1bil AUM with similar value investing tactics of previously mentioned mega investors

(opinion after attending iCapital Investor Day + researching on iCapital's historical investment style).

[iCapital.biz Bhd is a Malaysian listed public company managed by Capital Dynamics]

Fear not, for traders & bulls, this would be a great read - by Ken Fisher (Forbes 500 Investor) ;

http://www.forbes.com/sites/kenfisher/2014/10/15/the-secret-indicator-that-bulls-will-love/

In conclusion, look for companies bearing high dividends (min- market risk free rate:current MGS/ 10 year bond)

that have historically low prices NOT due to its core business or companies that are turning over a new leaf / to profitability (should you time this event well).

& maintain certain amount of CASH should you feel comforted in case of a correction you may get discounts all across the board. However, Mr Ken Fisher would tell you, comfort should not be inherent in investment management. For usually if you are comforted in making an investment decision, you would not make as well a decision as someone who wants to invest all his cash in stocks and still be able to withstand corrections.

A small confusion is always intended. Confusions will help us all develop our own personalized theories, philosophies and ideas in investing upon cracking our heads in making sense of everything.

Happy investing until next time.

US markets recently had a "10% correction" which should happen 1x annually (prior US gov intervention). This correction has occurred twice this year; in February and October. Can these corrections suffice for a 20% correction?

[relevant 10% correction article: http://www.cnbc.com/id/102106829]

Mr Buffett would rightly say always buy undervalued companies. In case of a further 20% correction (that used to occur every 3.5yrs that is long due now), your unrealised losses should your stock price accord the market, be minimal.

Hence, the answer would be maybe yes, maybe no.

Notice that all mega investors as such Mr Buffet, mr Li Ka Shing, Mr Al-Waleed bin Talal have all invested in undervalued companies successfully with a key ingredient. Cash.

During the roughest of times, they have all invested what cash they had accumulated into now cheap, quality stocks and companies.

In other words, they invest in cheap/undervalued companies all year round while keeping a good amount of cash in case of any market correction.

This is also the strategy of Tan Teng Boo the captain of Capital Dynamics, a closed end fund with about RM1bil AUM with similar value investing tactics of previously mentioned mega investors

(opinion after attending iCapital Investor Day + researching on iCapital's historical investment style).

[iCapital.biz Bhd is a Malaysian listed public company managed by Capital Dynamics]

Fear not, for traders & bulls, this would be a great read - by Ken Fisher (Forbes 500 Investor) ;

http://www.forbes.com/sites/kenfisher/2014/10/15/the-secret-indicator-that-bulls-will-love/

In conclusion, look for companies bearing high dividends (min- market risk free rate:current MGS/ 10 year bond)

that have historically low prices NOT due to its core business or companies that are turning over a new leaf / to profitability (should you time this event well).

& maintain certain amount of CASH should you feel comforted in case of a correction you may get discounts all across the board. However, Mr Ken Fisher would tell you, comfort should not be inherent in investment management. For usually if you are comforted in making an investment decision, you would not make as well a decision as someone who wants to invest all his cash in stocks and still be able to withstand corrections.

A small confusion is always intended. Confusions will help us all develop our own personalized theories, philosophies and ideas in investing upon cracking our heads in making sense of everything.

Happy investing until next time.

Wednesday, 24 September 2014

Properties

There will always be hot stocks, as such SHL CONSOLIDATED BHD. So, the question is do you buy it?

As usual, firstly, decide. Are you an investor (long term) or a trader (trader).

Upon deciding, notice that stocks of a particular sector usually move in tandem with one another. For example, property stocks have performed particularly well year to date (YTD), among others;

1) Titijaya Land Bhd

2) Eco World Development Group Bhd

3) Tambun Indah Land Bhd

4) SHL Consolidated Bhd

This particular nature of stock sector movement has been pointed out by Ken Fisher, a well known investment figure, also the descendant of Philip Arthur Fisher, a prolific investment theories contributor famous with the likes of Benjamin Graham.

The key factor is to not look at a particular stock, hot or not, but at the entire market and then a focused sector. For example, since the doldrums of cooling measures to be taken by the Malaysian government regarding property transactions began (end of 2013 into 2014), property stocks declined or stagnated (before the rally).

How is it then property stocks were one of the best performers?

Simple. Demand versus supply. According to rough statistics (usually presented in local media), there are roughly a few million buyers below the age of 37 looking to purchase a house, with an average annual household formation of 140,000 according to a property market report by the National Property Information Centre (Napic) found in a October 2013 article as below.

[http://www.thestar.com.my/business/sme/2013/10/17/many-reasons-for-rising-property-prices-in-msia-rehda-treasurer-says-supply-and-demand-is-most-signi/]

More actual statistics, new house prices increase about 10% yearly in major cities (meaning a gain of 10% annually on average for new buyers).

A consequent, local market love new properties. As leverage financing (a loan) helps an individual purchase a property as to which the developer bears the interest while the property is constructed and upon completion, the property can be sold for a handsome profit even after deducting real property gains tax (RPGT) and other penalty/cost.

[Note the mentioned Developer Interest Bearing Scheme (DIBS) is no longer allowed though companies are still offering them and RPGT % has been increased; these being part of the cooling measures initiated by the government]

Back to the companies mentioned. All had large projects that were launched end of 2013 and in 2014. The projects were sold out quite well as buyers bought into the rush prior cooling measures towards the end of 2013 and then more when cheaper projects like that of Titijaya were released besides the new buyers buying their first properties.

Note, we do not know whether the purchasers prior cooling measures were actual buyers or investors gobbling up many property at once (now a minimum imposed per individual).

This lack of data affects our idea on the market as a whole i.e. whether can buyers still afford houses and is the demand still strong enough to last (assuming a property bubble is brewing).

However, the companies, research reports and media, all would convince you the gross development value (GDV) of projects were substantial, there were good take up rates and hence good profits quarterly and great share price movement.

This sector performance was also due to the lagging nature of the sector as a whole and the smaller cap companies (Titijaya, SHL) that launched big projects finally obtained valuation similar to that given to its larger peers i.e. Mah Sing Group Bhd. In between, due to geopolitics concerns etc, the bigger cap property companies received attention for their more stable outlook due to their size and their launches.

Outlook: Companies developing cheaper range properties will continue to do well.

The property market globally tends to show Malaysian property market still has a long way to go. Consider Japan that has generationS servicing ONE loan. However, further cooling measures as such the likes of Singapore may slow down property prices whilst prospective buyers' income rise adequately to become actual buyers (assuming Malaysia's high income nation target is reached with higher REAL wages)

In conclusion, property companies should fare well for years to come as long they provide proper supply of what is in demand and maintaining/creating an efficient business model.

Until next time, happy investing.

[UPDATE (29/05/2015):

This is one of the better articles on Malaysian property sector found on TheEdgeMarkets.com

By Lam Jian Wyn / City & Country, The Edge Malaysia | May 28, 2015 : 8:00 PM MYT

http://www.theedgemarkets.com/my/article/edge-investment-forum-real-estate-2015-property-market-remain-cool-over-next-12-24-months

A short note: Investments should always suit investors' financial health, goals and psychology.]

As usual, firstly, decide. Are you an investor (long term) or a trader (trader).

Upon deciding, notice that stocks of a particular sector usually move in tandem with one another. For example, property stocks have performed particularly well year to date (YTD), among others;

1) Titijaya Land Bhd

2) Eco World Development Group Bhd

3) Tambun Indah Land Bhd

4) SHL Consolidated Bhd

This particular nature of stock sector movement has been pointed out by Ken Fisher, a well known investment figure, also the descendant of Philip Arthur Fisher, a prolific investment theories contributor famous with the likes of Benjamin Graham.

The key factor is to not look at a particular stock, hot or not, but at the entire market and then a focused sector. For example, since the doldrums of cooling measures to be taken by the Malaysian government regarding property transactions began (end of 2013 into 2014), property stocks declined or stagnated (before the rally).

How is it then property stocks were one of the best performers?

Simple. Demand versus supply. According to rough statistics (usually presented in local media), there are roughly a few million buyers below the age of 37 looking to purchase a house, with an average annual household formation of 140,000 according to a property market report by the National Property Information Centre (Napic) found in a October 2013 article as below.

[http://www.thestar.com.my/business/sme/2013/10/17/many-reasons-for-rising-property-prices-in-msia-rehda-treasurer-says-supply-and-demand-is-most-signi/]

More actual statistics, new house prices increase about 10% yearly in major cities (meaning a gain of 10% annually on average for new buyers).

A consequent, local market love new properties. As leverage financing (a loan) helps an individual purchase a property as to which the developer bears the interest while the property is constructed and upon completion, the property can be sold for a handsome profit even after deducting real property gains tax (RPGT) and other penalty/cost.

[Note the mentioned Developer Interest Bearing Scheme (DIBS) is no longer allowed though companies are still offering them and RPGT % has been increased; these being part of the cooling measures initiated by the government]

Back to the companies mentioned. All had large projects that were launched end of 2013 and in 2014. The projects were sold out quite well as buyers bought into the rush prior cooling measures towards the end of 2013 and then more when cheaper projects like that of Titijaya were released besides the new buyers buying their first properties.

Note, we do not know whether the purchasers prior cooling measures were actual buyers or investors gobbling up many property at once (now a minimum imposed per individual).

This lack of data affects our idea on the market as a whole i.e. whether can buyers still afford houses and is the demand still strong enough to last (assuming a property bubble is brewing).

However, the companies, research reports and media, all would convince you the gross development value (GDV) of projects were substantial, there were good take up rates and hence good profits quarterly and great share price movement.

This sector performance was also due to the lagging nature of the sector as a whole and the smaller cap companies (Titijaya, SHL) that launched big projects finally obtained valuation similar to that given to its larger peers i.e. Mah Sing Group Bhd. In between, due to geopolitics concerns etc, the bigger cap property companies received attention for their more stable outlook due to their size and their launches.

Outlook: Companies developing cheaper range properties will continue to do well.

The property market globally tends to show Malaysian property market still has a long way to go. Consider Japan that has generationS servicing ONE loan. However, further cooling measures as such the likes of Singapore may slow down property prices whilst prospective buyers' income rise adequately to become actual buyers (assuming Malaysia's high income nation target is reached with higher REAL wages)

In conclusion, property companies should fare well for years to come as long they provide proper supply of what is in demand and maintaining/creating an efficient business model.

Until next time, happy investing.

[UPDATE (29/05/2015):

This is one of the better articles on Malaysian property sector found on TheEdgeMarkets.com

By Lam Jian Wyn / City & Country, The Edge Malaysia | May 28, 2015 : 8:00 PM MYT

http://www.theedgemarkets.com/my/article/edge-investment-forum-real-estate-2015-property-market-remain-cool-over-next-12-24-months

A short note: Investments should always suit investors' financial health, goals and psychology.]

Thursday, 28 August 2014

Research Reports Parkson

[Part 2]

The final comparison.

Consider the reports on the 27th of August in particular regarding the sale announcement of KL Festival City Mall (available at http://klse.i3investor.com/servlets/ptg/5657.jsp). Compare reports with price targets of RM2.51 and rm3.85 respectively.

One report reports the sale will garner "an exceptional gain or 10 sen/share" of RM110mil for shareholders

The other reports "cash pile will be boosted by the sale for RM349mil"

Notice abysmal the difference a singular announcement above affected the price target given by each financial house & the difference in tone (negative,positive).

[Interestingly: The media can chose either report to publish i.e. via newspapers]

In conclusion, to estimate a price that will be paid by future buyers (of a stock), one can look at a particular market's favorite method of evaluation.

For e.g. it is more likely that a company in Malaysia will use the following:

1) P/E ratio

2) Net Profit growth rate (%)

3) Revenue growth rate (%)

4) Net Asset Value (NAV) / Net Tangible Assets (NTA)

as the main evaluation metric.

The above plus peer comparison (comparing companies of similar nature) should allow for a relatively good future projection of a company's stock performance.

Of course the above qualitative methods should also have added quantitative measures as such; is it a favored stock, does it carry a premium due to a fantastic management/business model, will there be more satisfied customers years onward, and much more.

[Note: Evaluations - Most companies i.e. Oldtown bhd & Sch Bhd that have great balance sheets with very low debt usually causes less attractive evaluations. Why? For instance, Oldtown Bhd. Revenue generated is used to finance debt hence reducing its net profits which affects all the 4 evaluation metric stated above. This is contrasted to companies in the US that use debt (e.g. bonds) to finance debt (NOT Cost to produce goods/services) to improve evaluations since debt and net profit fall into seperate categories].

Until next time, happy investing.

The final comparison.

Consider the reports on the 27th of August in particular regarding the sale announcement of KL Festival City Mall (available at http://klse.i3investor.com/servlets/ptg/5657.jsp). Compare reports with price targets of RM2.51 and rm3.85 respectively.

One report reports the sale will garner "an exceptional gain or 10 sen/share" of RM110mil for shareholders

The other reports "cash pile will be boosted by the sale for RM349mil"

Notice abysmal the difference a singular announcement above affected the price target given by each financial house & the difference in tone (negative,positive).

[Interestingly: The media can chose either report to publish i.e. via newspapers]

In conclusion, to estimate a price that will be paid by future buyers (of a stock), one can look at a particular market's favorite method of evaluation.

For e.g. it is more likely that a company in Malaysia will use the following:

1) P/E ratio

2) Net Profit growth rate (%)

3) Revenue growth rate (%)

4) Net Asset Value (NAV) / Net Tangible Assets (NTA)

as the main evaluation metric.

The above plus peer comparison (comparing companies of similar nature) should allow for a relatively good future projection of a company's stock performance.

Of course the above qualitative methods should also have added quantitative measures as such; is it a favored stock, does it carry a premium due to a fantastic management/business model, will there be more satisfied customers years onward, and much more.

[Note: Evaluations - Most companies i.e. Oldtown bhd & Sch Bhd that have great balance sheets with very low debt usually causes less attractive evaluations. Why? For instance, Oldtown Bhd. Revenue generated is used to finance debt hence reducing its net profits which affects all the 4 evaluation metric stated above. This is contrasted to companies in the US that use debt (e.g. bonds) to finance debt (NOT Cost to produce goods/services) to improve evaluations since debt and net profit fall into seperate categories].

Until next time, happy investing.

Thursday, 21 August 2014

Research Reports Parkson

[Part 1]

Parkson Holdings Bhd (parent company) is taken as a case study to test the viability of Research Reports (RRs).

It is recommended (as previously mentioned) that Research Reports should only COMPLEMENT own research done via analysing company announcements via 1st party documentation; by the company itself or through informed source(s).

RRs on Parkson dated 20/08/2014:

( 3 main RR released: http://klse.i3investor.com/servlets/ptg/5657.jsp including RR posted at http://www.bursamalaysia.com/market/listed-companies/list-of-companies/plc-profile.html?stock_code=5657 )

In brief, it is assumed the RRs was a respond to Parkson's disposal of its fully owned KL Festival City Mall (henceforth the Property) for RM349mil to Festiva Mall Sdn Bhd with AsiaMalls Sdn Bhd being the holding company.

This would unlock RM349mil (initial purchase price of RM246mil + RM103mil of profit from disposal) to be used as per reported by Parkson Bhd:

[RM200mil]; General investments including acquisition, development and management of retail malls and Working capital

[RM100mil]; Expenses related to the Proposed Disposal

Firstly, Parkson's anchor tenancy business within the Property will go on as usual.

Secondly, unlocking cash value is always good for any company, if sufficient cash is raised (appraised market value of the Property: RM353.8mil by Henry Butcher Malaysia Sdn Bhd) and an adequate return on invested capital (ROIC). Parkson's main ideology is to grow with internally generated funds with the least usage of debt. Although a rough calculation of ROIC from the mentioned disposal is difficult, it is assumed from Parkson's ideology and transparent book keeping, the cash to be raised will give a sufficient return in share value.

[ ROIC: a Company's efficiency in allocating capital. More at

http://www.investopedia.com/terms/r/returnoninvestmentcapital.asp ]

ROIC % and in turn a theoratical Internal Rate of Return (IRR) for individual shareholders is enhanced in view of retail space that is increasing in Kuala Lumpur and the reinvestment of cash in other outlets in/future development i.e. in Melaka, a still under developed city in terms of retail business.

Thirdly, in simplistic terms;

1) The cash due RM349mil upon completion of the conditional Sale & Purchase (S&P) in approximately 1-2 months will enhance Parkson's balance sheet by RM349mil or RM200mil assuming cost of disposal=RM149mil.

2) This will increase Parkson's valuations for Year 2014 unless the next 2 quarters of shopping season does really badly (the 1st half was relatively good).

Assuming negative valuations are produced by RRs, the cash will be utilized for future stores which should be fully owned by Parkson without incurring debt to grow elsewhere.

[Note: More than 65-75% of revenue is generated by Parkson Retail Group operating in a strong consumers market- China, with stiff competition that seems to be growing on debt i.e. Intime Retail Group Co Ltd and Golden Eagle Retail Group Ltd]

Fourthly, Parkson Retail Asia Limited, the Singapore subsidiary is to report its quarterly report today 21/08/2014 (after trading period).

The RRs seem to suggest Parkson will be moving no where for now, but the incoming cash flow and the business structure of anchor tenancy for the next two or more quarters seems to be vagrantly positive.

Well, in short, RRs exists only to persuade purchases for institutional funds /investors have their own qualification to purchase stocks in which one believes have all been met by the recent asset disposal.

[Fun Fact: the Disposal was a surprise in one RR and not at all to another]

There are many more considerations to valuing a company than what RRs have to offer. Besides, without such reports, those who produce them might lose credibility and goodwill. Hence, the need to constantly revise their stand to remain relevant and in business.

[Interestingly: The RRs often display a word for word reproduction of company announcements with added short term opinions]

In conclusion, use RRs wisely for despite the above, they give a quick outlook for any given company.

Happy investing.

Parkson Holdings Bhd (parent company) is taken as a case study to test the viability of Research Reports (RRs).

It is recommended (as previously mentioned) that Research Reports should only COMPLEMENT own research done via analysing company announcements via 1st party documentation; by the company itself or through informed source(s).

( 3 main RR released: http://klse.i3investor.com/servlets/ptg/5657.jsp including RR posted at http://www.bursamalaysia.com/market/listed-companies/list-of-companies/plc-profile.html?stock_code=5657 )

In brief, it is assumed the RRs was a respond to Parkson's disposal of its fully owned KL Festival City Mall (henceforth the Property) for RM349mil to Festiva Mall Sdn Bhd with AsiaMalls Sdn Bhd being the holding company.

This would unlock RM349mil (initial purchase price of RM246mil + RM103mil of profit from disposal) to be used as per reported by Parkson Bhd:

[RM200mil]; General investments including acquisition, development and management of retail malls and Working capital

[RM100mil]; Expenses related to the Proposed Disposal

Firstly, Parkson's anchor tenancy business within the Property will go on as usual.

Secondly, unlocking cash value is always good for any company, if sufficient cash is raised (appraised market value of the Property: RM353.8mil by Henry Butcher Malaysia Sdn Bhd) and an adequate return on invested capital (ROIC). Parkson's main ideology is to grow with internally generated funds with the least usage of debt. Although a rough calculation of ROIC from the mentioned disposal is difficult, it is assumed from Parkson's ideology and transparent book keeping, the cash to be raised will give a sufficient return in share value.

[ ROIC: a Company's efficiency in allocating capital. More at

http://www.investopedia.com/terms/r/returnoninvestmentcapital.asp ]

ROIC % and in turn a theoratical Internal Rate of Return (IRR) for individual shareholders is enhanced in view of retail space that is increasing in Kuala Lumpur and the reinvestment of cash in other outlets in/future development i.e. in Melaka, a still under developed city in terms of retail business.

Thirdly, in simplistic terms;

1) The cash due RM349mil upon completion of the conditional Sale & Purchase (S&P) in approximately 1-2 months will enhance Parkson's balance sheet by RM349mil or RM200mil assuming cost of disposal=RM149mil.

2) This will increase Parkson's valuations for Year 2014 unless the next 2 quarters of shopping season does really badly (the 1st half was relatively good).

Assuming negative valuations are produced by RRs, the cash will be utilized for future stores which should be fully owned by Parkson without incurring debt to grow elsewhere.

[Note: More than 65-75% of revenue is generated by Parkson Retail Group operating in a strong consumers market- China, with stiff competition that seems to be growing on debt i.e. Intime Retail Group Co Ltd and Golden Eagle Retail Group Ltd]

Fourthly, Parkson Retail Asia Limited, the Singapore subsidiary is to report its quarterly report today 21/08/2014 (after trading period).

The RRs seem to suggest Parkson will be moving no where for now, but the incoming cash flow and the business structure of anchor tenancy for the next two or more quarters seems to be vagrantly positive.

Well, in short, RRs exists only to persuade purchases for institutional funds /investors have their own qualification to purchase stocks in which one believes have all been met by the recent asset disposal.

[Fun Fact: the Disposal was a surprise in one RR and not at all to another]

There are many more considerations to valuing a company than what RRs have to offer. Besides, without such reports, those who produce them might lose credibility and goodwill. Hence, the need to constantly revise their stand to remain relevant and in business.

[Interestingly: The RRs often display a word for word reproduction of company announcements with added short term opinions]

In conclusion, use RRs wisely for despite the above, they give a quick outlook for any given company.

Happy investing.

Monday, 7 July 2014

Investors according to Benjamin Graham

First, who is Benjamin Graham? A quick google search will probably show you an excellent investor ahead of his time back in 1930s whom have recorded the investment psychology of investors which has not changed much in over 80 years. Even Warren Buffett would swear by Graham's evaluation techniques and logical deductions, all made available in the famous books, The Intelligent Investor and Security Analysis.

Surely then this man, a forerunner of ACCA had to know a thing or two about investing. Hence, most articles posted on this blog tries to assimilate their investment wisdom. Thus, reading the two books mentioned is deemed priceless for investment analysis.

A quote by Benjamin Graham.

"A True Investor is scarcely ever forced to sell his shares & free to disregard current price quotation. He only need pay attention to selling at favorable price. Thus, investor who permits himself to be stampeded or unduly worried by unjustified market declines in his holdings is perversely transforming his basic advantage into his basic disadvantage. That man would be better of if his stocks had no market quotation at all for then he would be spared the mental anguish caused by other persons mistakes of judgement."

His general main idea of securities investment is among others, buying securities/shares of company(s) that have strong earnings, commendable market share, low debt and one that should be around for a long time to come.

A current day flavour of Value Investing, a term most associated with Graham, can also be attained from materials linked to Professor Bruce Greenwald, a Columbia Business School professor.

Until next time, happy investing.

Surely then this man, a forerunner of ACCA had to know a thing or two about investing. Hence, most articles posted on this blog tries to assimilate their investment wisdom. Thus, reading the two books mentioned is deemed priceless for investment analysis.

A quote by Benjamin Graham.

"A True Investor is scarcely ever forced to sell his shares & free to disregard current price quotation. He only need pay attention to selling at favorable price. Thus, investor who permits himself to be stampeded or unduly worried by unjustified market declines in his holdings is perversely transforming his basic advantage into his basic disadvantage. That man would be better of if his stocks had no market quotation at all for then he would be spared the mental anguish caused by other persons mistakes of judgement."

His general main idea of securities investment is among others, buying securities/shares of company(s) that have strong earnings, commendable market share, low debt and one that should be around for a long time to come.

A current day flavour of Value Investing, a term most associated with Graham, can also be attained from materials linked to Professor Bruce Greenwald, a Columbia Business School professor.

Until next time, happy investing.

New IPOs

Lock Up Periods / Moratorium

Lock ups or moratorium are periods within which initial investors, those whom have purchased shares prior listing, are NOT allowed to sell legally. They may sell their shares after the stipulated period (based on individual company lock up/tie up period/moratorium agreement). For example, Twitter shares which was listed in the States had a fall in share price as soon as the lock up period was over recently as initial investor could finally lock in their profits by selling their shares (have since seen a rise in share price).

New companies such as Icon Offshore Bhd and Boustead Plantations Bhd and all others in Malaysia do not have lock up periods. Thus, "cornerstone investors" as they are frequently labelled may sell their positions as soon as these companies are listed.

In wrought conclusion, speculation may peak on listing day for any given IPOs. Thus, a fall in price should not discourage investors. Though having analysed the prospectus adequately might prove beneficial to buy into the drop in prices. The perfect example would have been Titijaya Bhd in the earlier half of 2014.

However, this is a rough analysis of the 2 mentioned new companies. Icon Offshore was previously the offshore related division (OSV) of Tanjung Offshore Bhd, now listed as a separate company specializing in offshore related activities (OSV). It also has EKUINAS as one of their major shareholder. Considering its ties to EKUINAS, it is projected that this company will successfully capitalize new funds garnered from listing to expand its business through government related contracts. And for your information, this company was previously known as Tanjung Kapal Services Sdn. Bhd.

According to a self survey, it is seen that most IPOs since the 4th quarter of 2013 until present 2014 3rd quarter have seen a relatively good increase in share price on average. Namely due to listing requirements by Securities Commission Malaysia and Bursa Malaysia that are conservative in nature relative to the States & the paring down of debts, increase in capex / assets / etc via listing capital, communing better evaluations in research reports produced by banks and other institutions.

Despite the above, it is to be noted the number of times Boustead Plantations have been listed, delisted and re-listed & the acres of new plantation that have matured as compared to total new plantation area. It is opined new funds will be used to make land acquisitions at a relatively diluted value per shareholding due to current total shares issued and held by major corporation/individual.

In terms of investment, acquiring agricultural land personally/collectively with partner(s), if financially viable, and contracting it out to garner returns would seem the better choice, assuming land is bought in areas targeted by the company mentioned. A return in crops of above 15% on contract may give a 10% return if financed by a 4% interest bearing loan. There are many specially available loans provided by banks (i.e. SME Bank) & government related sources currently.

The key is finding a value for money investment. Agricultural land can still be acquired in certain regions for low prices relative to their earning capacity.

Therefore, capitalise wisely and happy investing.

[Please note: These are all opinions and are not intended to be used as advice for investment purposes until and unless proper evaluations are conducted personally according to individual financial means, upon which liability is fully borne by the decision maker]

Lock ups or moratorium are periods within which initial investors, those whom have purchased shares prior listing, are NOT allowed to sell legally. They may sell their shares after the stipulated period (based on individual company lock up/tie up period/moratorium agreement). For example, Twitter shares which was listed in the States had a fall in share price as soon as the lock up period was over recently as initial investor could finally lock in their profits by selling their shares (have since seen a rise in share price).

New companies such as Icon Offshore Bhd and Boustead Plantations Bhd and all others in Malaysia do not have lock up periods. Thus, "cornerstone investors" as they are frequently labelled may sell their positions as soon as these companies are listed.

In wrought conclusion, speculation may peak on listing day for any given IPOs. Thus, a fall in price should not discourage investors. Though having analysed the prospectus adequately might prove beneficial to buy into the drop in prices. The perfect example would have been Titijaya Bhd in the earlier half of 2014.

However, this is a rough analysis of the 2 mentioned new companies. Icon Offshore was previously the offshore related division (OSV) of Tanjung Offshore Bhd, now listed as a separate company specializing in offshore related activities (OSV). It also has EKUINAS as one of their major shareholder. Considering its ties to EKUINAS, it is projected that this company will successfully capitalize new funds garnered from listing to expand its business through government related contracts. And for your information, this company was previously known as Tanjung Kapal Services Sdn. Bhd.

According to a self survey, it is seen that most IPOs since the 4th quarter of 2013 until present 2014 3rd quarter have seen a relatively good increase in share price on average. Namely due to listing requirements by Securities Commission Malaysia and Bursa Malaysia that are conservative in nature relative to the States & the paring down of debts, increase in capex / assets / etc via listing capital, communing better evaluations in research reports produced by banks and other institutions.

Despite the above, it is to be noted the number of times Boustead Plantations have been listed, delisted and re-listed & the acres of new plantation that have matured as compared to total new plantation area. It is opined new funds will be used to make land acquisitions at a relatively diluted value per shareholding due to current total shares issued and held by major corporation/individual.

In terms of investment, acquiring agricultural land personally/collectively with partner(s), if financially viable, and contracting it out to garner returns would seem the better choice, assuming land is bought in areas targeted by the company mentioned. A return in crops of above 15% on contract may give a 10% return if financed by a 4% interest bearing loan. There are many specially available loans provided by banks (i.e. SME Bank) & government related sources currently.

The key is finding a value for money investment. Agricultural land can still be acquired in certain regions for low prices relative to their earning capacity.

Therefore, capitalise wisely and happy investing.

[Please note: These are all opinions and are not intended to be used as advice for investment purposes until and unless proper evaluations are conducted personally according to individual financial means, upon which liability is fully borne by the decision maker]

Wednesday, 18 June 2014

Where to get STOCK INFORMATION?

These are a few links that will take you to free stock data of any shares you are looking at. It should contain share price, P/E values, total shares issue, historical prices, financial overlook, financial ratios and much more.

Malaysian Stocks

Bursa Malaysia

http://www.bursamalaysia.com/market/

[Type in the stock name in the "Get Quote" box on the top right centre of the page. Then choose "Company Information" from a list that will appear next to the chosen stock. Reload page if it doesn't show any results]

Comment: Good information. Beware, vital stock announcement delayed sometimes (common)

E.g. stock quote page : http://www.bursamalaysia.com/market/listed-companies/list-of-companies/plc-profile.html?stock_code=5657

Malaysiastock.biz

http://www.malaysiastock.biz/Latest-Announcement.aspx

[Same as above]

Comment : Good information on revenue & profit trend, quarter report history, dividend history, bonus/right issue history all in 1 PAGE

E.g. stock quote page : http://www.malaysiastock.biz/Corporate-Infomation.aspx?type=A&value=P&source=M&securityCode=5657

Stock Price Target by Banks

http://klse.i3investor.com/jsp/pt.jsp

[Same as above]

Comment : All bank reports are Revised according to Latest Financial/pertinent data. Do not use this as a primary criteria. However, they give an overlook of a company's Current well being

E.g. stock quote page : http://klse.i3investor.com/servlets/ptg/5657.jsp

Malaysian & International stocks

Financial Times

http://www.ft.com/home/asia

[Same as above]

Comment : Great overall view for any particular aspect

E.g stock quote : http://markets.ft.com/research/Markets/Tearsheets/Summary?s=PARKSON:KLS

Reuters

http://www.reuters.com

[Same as above]

Comment : Good "Overview" page

E.g. stock quote page : http://www.reuters.com/finance/stocks/overview?symbol=PRKN.KL

Bloomberg

http://www.bloomberg.com/quote/PKS:MK

[Same as above]

E.g. stock quote page : http://www.bloomberg.com/quote/PKS:MK

For FAST SEARCHES:

Go to Google.com, type in the name of your stock followed by the website (any one of the above you want to use, except for bursamalaysia)

E.g.

For information on Parkson Bhd,

type in "parkson bhd bloomberg/reuters/ft" and click on your search result.

This is the fastest way of getting to your the free websites quoted above.

These websites are extremely helpful to give you numbers conducted by banks/analysts/etc. However, I would recommend to use your own research data and use the above only as pussuasive authority. There are many other websites such as WSJ

(e.g. http://online.wsj.com/quotes/stock_charting.html?symbol=3368&type=hkse&osymb=HK-jB3368&x=44&y=18&time=2yr&freq=1dy&wtype=64&compidx=&comp=&ma=1&maval=200&uf=0&sid=2156591&symb=HK-jB3368&lf=268435456&lf2=0&lf3=0)

that provide stock charting with buy & sell volume : Volume+ , amongst others.

Use the above fast search technique for them too if extra information is required.

Until next time, happy investing.

P.s. I am not directly recommending the purchase of Parkson Bhd shares. It is just an example.

Malaysian Stocks

Bursa Malaysia

http://www.bursamalaysia.com/market/

[Type in the stock name in the "Get Quote" box on the top right centre of the page. Then choose "Company Information" from a list that will appear next to the chosen stock. Reload page if it doesn't show any results]

Comment: Good information. Beware, vital stock announcement delayed sometimes (common)

E.g. stock quote page : http://www.bursamalaysia.com/market/listed-companies/list-of-companies/plc-profile.html?stock_code=5657

Malaysiastock.biz

http://www.malaysiastock.biz/Latest-Announcement.aspx

[Same as above]

Comment : Good information on revenue & profit trend, quarter report history, dividend history, bonus/right issue history all in 1 PAGE

E.g. stock quote page : http://www.malaysiastock.biz/Corporate-Infomation.aspx?type=A&value=P&source=M&securityCode=5657

Stock Price Target by Banks

http://klse.i3investor.com/jsp/pt.jsp

[Same as above]

Comment : All bank reports are Revised according to Latest Financial/pertinent data. Do not use this as a primary criteria. However, they give an overlook of a company's Current well being

E.g. stock quote page : http://klse.i3investor.com/servlets/ptg/5657.jsp

Malaysian & International stocks

Financial Times

http://www.ft.com/home/asia

[Same as above]

Comment : Great overall view for any particular aspect

E.g stock quote : http://markets.ft.com/research/Markets/Tearsheets/Summary?s=PARKSON:KLS

Reuters

http://www.reuters.com

[Same as above]

Comment : Good "Overview" page

E.g. stock quote page : http://www.reuters.com/finance/stocks/overview?symbol=PRKN.KL

Bloomberg

http://www.bloomberg.com/quote/PKS:MK

[Same as above]

E.g. stock quote page : http://www.bloomberg.com/quote/PKS:MK

For FAST SEARCHES:

Go to Google.com, type in the name of your stock followed by the website (any one of the above you want to use, except for bursamalaysia)

E.g.

For information on Parkson Bhd,

type in "parkson bhd bloomberg/reuters/ft" and click on your search result.

This is the fastest way of getting to your the free websites quoted above.

These websites are extremely helpful to give you numbers conducted by banks/analysts/etc. However, I would recommend to use your own research data and use the above only as pussuasive authority. There are many other websites such as WSJ

(e.g. http://online.wsj.com/quotes/stock_charting.html?symbol=3368&type=hkse&osymb=HK-jB3368&x=44&y=18&time=2yr&freq=1dy&wtype=64&compidx=&comp=&ma=1&maval=200&uf=0&sid=2156591&symb=HK-jB3368&lf=268435456&lf2=0&lf3=0)

that provide stock charting with buy & sell volume : Volume+ , amongst others.

Use the above fast search technique for them too if extra information is required.

Until next time, happy investing.

P.s. I am not directly recommending the purchase of Parkson Bhd shares. It is just an example.

Wednesday, 11 June 2014

Ecoworld - Buy or Sell?

Ecoworld

A "spinoff" of S P Setia? Perhaps. This would mean there is a new but old company trying to raise more public money to develop more land, purchased at low prices and sold to would be property investor for extravagant price (land has been purchased before from Tropicana from the government for a very modest price).

Back to share investment in Ecoworld. Current share price : RM5.07. So what do you get from this price. These are among the proposed exercises and brief explanations.

1) share split for shareholders :

"Upon completion of the Proposed Share Split, the issued and paid-up share capital of EW Berhad would be RM253,317,000 comprising 506,634,000 ordinary shares of RM0.50 each"

Current par value shares of RM1 becomes 2 shares of a par value of RM0.50 (par value : initial capital injected by the company) hence value of 2 new shares still = 1 share held previously

2) private placement via Share Subcription :

"Pursuant to the Share Subscription Agreement, EW Holdings and Sinarmas Harta (collectively referred to as the “Subscribers”) will subscribe for new EW Berhad Shares for an aggregate cash consideration of RM1,371,639,648.40 (“Subscription Consideration”) at an issue price of RM1.70 for each Subscription Share (“Subscription Issue Price”) "

Hence, the mentioned Subscribers will own 806,846,852 shares or 61.42% of the total share issue after the proposed split.

3) share subscription for shareholders via Rights issue shares with free detachable warrants

The above private placement will dilute current public shareholding from 34.95% to 13.48%. Every public company is required to have 25% in the hands of the public (hence "Public" Company). Hence, this exercise is necessary for the company to remain a public company (in the process raising RM788,000,000, before the warrants are exercised, for repayment of bank loans and future land acquisition). This is beneficial for shareholders as long as the rights price matches that of EW Holdings and Sinarmas Harta. If not, your share value will be diluted.

[rights: shares (quantity depending on current no. Of shares held) offered at a lower price

Warrants: depending on type. Convertible to shares / Detachable-can be sold separately]

4) further Private placement

The Proposed Placement will involve the placement of such number of new EW Berhad Shares, representing up to 20% of the existing issued and paid-up share capital of EW Berhad post completion of the Proposed Share Subscription and Proposed Rights Issue with Warrants (“Placement Shares”) to investors to be identified via a book-building exercise at an issue price to be determined (“Placement Issue Price”).

In short: The above proposals will cause a Dilution effect of 41.56% OR in other words, you will retain a value of 58.44% of your current shares assuming you fully subscribe to the proposed Rights issue and are able to exercise all of your free warrants.

The above number is generated from taking the total number of shares after the relevant proposals for shareholders, divided by the total number of shares after adding shares to be issued to private individuals/corporation.

A small discussion. Ecoworld is a land development company that is about to raise sufficient cash for future developments. As a shareholder, it is crucial to know whether this company will pay sufficient dividends to substantiate the dilution that is about to occur. Not to forgo the value of the company presently and post proposed corporate actions. Assuming the company generates RM2bil for the year 2014, with a net profit of RM200mil, a P/E ratio of 36x is estimated for post corporate actions with current share price, assuming full public float.

It is estimated the P/E to be about 15-30 if net profits are higher and dilution occurs at a slow pace. This would put the company's valuation alongside other large developers or cheaper allowing for capital appreciation.

Not to forget other considerations, such as cash flow, debts, etc. However, it is opined that the major influence on share price for large cap companies in Malaysia is the pension fund and other large institution. As long as this Ecoworld sells its products and continue growing its land banks, it would seem that it's share price will continue to appreciate [assuming ESOS and other future proposals does not further dilute public shareholder's stake].

A continuous and/or dilution effects is contrary to safeguarding shareholders interest. After all, shouldn't public companies benefit public instead of private individuals via private placements amongst others? However, a company that does not care for its public shareholders, may still be a good investment assuming it continues to deliver performance.

It is extremely common that companies grow without benefitting the public shareholders. Hence, having a management team that focuses on shareholder value is priceless. Not having this would lead to the paradox of striving to generate profits and concurrently not wanting to be made used of.

Conclusion. If a company provides opportunity for capital appreciation, it should also provide some sort of guarantee in maintaining your capital value. Supporting companies with pure greed for returns may backfire in other ways, perhaps general increases in property price.

[I will recommend a Buy for the long term if you have some extra cash lying around]

Reminder: Investment should be for the longer term. A suggestion, if you have RM10000, spend half and keep 25% x 2 (RM2500 x 2) for back up in case the share price dips (many purchases=larger purchase costs). In the long run, assuming the company focuses on shareholder value, has a great brand, cash flow, balance sheet & pays dividends (if possible equal to that of bank interest rate), you will do well.

Until next time happy investing.

A "spinoff" of S P Setia? Perhaps. This would mean there is a new but old company trying to raise more public money to develop more land, purchased at low prices and sold to would be property investor for extravagant price (land has been purchased before from Tropicana from the government for a very modest price).

Back to share investment in Ecoworld. Current share price : RM5.07. So what do you get from this price. These are among the proposed exercises and brief explanations.

1) share split for shareholders :

"Upon completion of the Proposed Share Split, the issued and paid-up share capital of EW Berhad would be RM253,317,000 comprising 506,634,000 ordinary shares of RM0.50 each"

Current par value shares of RM1 becomes 2 shares of a par value of RM0.50 (par value : initial capital injected by the company) hence value of 2 new shares still = 1 share held previously

2) private placement via Share Subcription :

"Pursuant to the Share Subscription Agreement, EW Holdings and Sinarmas Harta (collectively referred to as the “Subscribers”) will subscribe for new EW Berhad Shares for an aggregate cash consideration of RM1,371,639,648.40 (“Subscription Consideration”) at an issue price of RM1.70 for each Subscription Share (“Subscription Issue Price”) "

Hence, the mentioned Subscribers will own 806,846,852 shares or 61.42% of the total share issue after the proposed split.

3) share subscription for shareholders via Rights issue shares with free detachable warrants

The above private placement will dilute current public shareholding from 34.95% to 13.48%. Every public company is required to have 25% in the hands of the public (hence "Public" Company). Hence, this exercise is necessary for the company to remain a public company (in the process raising RM788,000,000, before the warrants are exercised, for repayment of bank loans and future land acquisition). This is beneficial for shareholders as long as the rights price matches that of EW Holdings and Sinarmas Harta. If not, your share value will be diluted.

[rights: shares (quantity depending on current no. Of shares held) offered at a lower price

Warrants: depending on type. Convertible to shares / Detachable-can be sold separately]

4) further Private placement

The Proposed Placement will involve the placement of such number of new EW Berhad Shares, representing up to 20% of the existing issued and paid-up share capital of EW Berhad post completion of the Proposed Share Subscription and Proposed Rights Issue with Warrants (“Placement Shares”) to investors to be identified via a book-building exercise at an issue price to be determined (“Placement Issue Price”).

In short: The above proposals will cause a Dilution effect of 41.56% OR in other words, you will retain a value of 58.44% of your current shares assuming you fully subscribe to the proposed Rights issue and are able to exercise all of your free warrants.

The above number is generated from taking the total number of shares after the relevant proposals for shareholders, divided by the total number of shares after adding shares to be issued to private individuals/corporation.

A small discussion. Ecoworld is a land development company that is about to raise sufficient cash for future developments. As a shareholder, it is crucial to know whether this company will pay sufficient dividends to substantiate the dilution that is about to occur. Not to forgo the value of the company presently and post proposed corporate actions. Assuming the company generates RM2bil for the year 2014, with a net profit of RM200mil, a P/E ratio of 36x is estimated for post corporate actions with current share price, assuming full public float.

It is estimated the P/E to be about 15-30 if net profits are higher and dilution occurs at a slow pace. This would put the company's valuation alongside other large developers or cheaper allowing for capital appreciation.

Not to forget other considerations, such as cash flow, debts, etc. However, it is opined that the major influence on share price for large cap companies in Malaysia is the pension fund and other large institution. As long as this Ecoworld sells its products and continue growing its land banks, it would seem that it's share price will continue to appreciate [assuming ESOS and other future proposals does not further dilute public shareholder's stake].

A continuous and/or dilution effects is contrary to safeguarding shareholders interest. After all, shouldn't public companies benefit public instead of private individuals via private placements amongst others? However, a company that does not care for its public shareholders, may still be a good investment assuming it continues to deliver performance.

It is extremely common that companies grow without benefitting the public shareholders. Hence, having a management team that focuses on shareholder value is priceless. Not having this would lead to the paradox of striving to generate profits and concurrently not wanting to be made used of.

Conclusion. If a company provides opportunity for capital appreciation, it should also provide some sort of guarantee in maintaining your capital value. Supporting companies with pure greed for returns may backfire in other ways, perhaps general increases in property price.

[I will recommend a Buy for the long term if you have some extra cash lying around]

Reminder: Investment should be for the longer term. A suggestion, if you have RM10000, spend half and keep 25% x 2 (RM2500 x 2) for back up in case the share price dips (many purchases=larger purchase costs). In the long run, assuming the company focuses on shareholder value, has a great brand, cash flow, balance sheet & pays dividends (if possible equal to that of bank interest rate), you will do well.

Until next time happy investing.

Sunday, 27 April 2014

Speculation Vs Investment

Trading is speculation whereby you buy and sell stocks for short term gains. Speculation is when you buy something without solid justified reasons.

For example, PBA Bhd shares as of late suddenly had a surge in price upon news of high chances of a rate hike. The higher share price now can only be justified as an "investment" if;

1) the rate hike is executed

2) the current price does not yet reflect an increase profits to be realized

3) etc.

PBA graph:

[http://www.bursamalaysia.com/market/listed-companies/list-of-companies/plc-profile.html?stock_code=5041]

However, a bursa Malaysia graph of PBA would show a price movement from RM1.16 to RM1.65, beginning of April to its peak towards the end of the month. That is a 42% increase. Could the new rates YET to be implemented have a 42% increase in profits (assuming the company is worth RM1.16 as of end of March 2014) ? And if the answer is yes, will the profit be distributed to the shareholders via dividends amongst other ways?

A simple solution, have a look at this digram (nicknamed Trader's Graph)

[http://www.businessinsider.com/how-not-to-invest-2014-4?IR=T&]

I'm sure many if us can relate to this diagram for it shows when most traders execute their trades. Of course there will be a small number of successful traders that had the mental (& financial) stretch to make use of such news-caused-fluctuation-effect.

Studying PBA's graph and also another, Datasonic Bhd would show a proper method for traders: Buying after a 'sudden decrease' in price. However so, note that such a method can prove unsuccessful if the company traded Stops giving out Exciting news.

Despite the above, it is seen that a purchase on a upward trend is most likely to give negative results if the trader fails to sell "in time". When is it time then? Well, there is no answer to this question but this remains the highest contributor to non successful trading and a cause of mental stress, sleep disorder and other anxiety related problems.

[Interestingly, insider trading is the best form for successful trading. However, it is illegal but note, with low conviction rate]

Datasonic is a great case study. An initial price of just above RM2 in May 2013, a high of RM10 at the end of 2013, share split, then an increase back to a high of RM4.87, then a sudden drop of 26% to RM3.58, a rise back to RM3.91 followed by a 27% drop to RM2.85. In short, the investor for the long term (May 2013-May 2014) would have reaped a gain of approximately 1200%. This company has one of the highest 1 year return stock. Despite the gains, if one observed the Trader's Graph, many would have fell into a disfavourable situation for investments made in 2014 (due to the warrants exercised and sale by those reaping their huge returns) until new Exciting news emerged yet again.

On an investment basis, it is least mentally taxing and financially beneficial to purchase stocks that have value; the means to continue successful operations at a low price that distributes profits generated to shareholders - the rightful owners of "Public" companies and recognises shareholders contribution (by not making unfavorable deals that would undermine shareholders). Businesses finance expansions via shareholders contribution thus it is only natural for the above suggestions.

This is rather a short post, for the Trader's Graph above summed up quite a lot.

Happy investing till next time.

For example, PBA Bhd shares as of late suddenly had a surge in price upon news of high chances of a rate hike. The higher share price now can only be justified as an "investment" if;

1) the rate hike is executed

2) the current price does not yet reflect an increase profits to be realized

3) etc.

PBA graph:

[http://www.bursamalaysia.com/market/listed-companies/list-of-companies/plc-profile.html?stock_code=5041]

However, a bursa Malaysia graph of PBA would show a price movement from RM1.16 to RM1.65, beginning of April to its peak towards the end of the month. That is a 42% increase. Could the new rates YET to be implemented have a 42% increase in profits (assuming the company is worth RM1.16 as of end of March 2014) ? And if the answer is yes, will the profit be distributed to the shareholders via dividends amongst other ways?

A simple solution, have a look at this digram (nicknamed Trader's Graph)

[http://www.businessinsider.com/how-not-to-invest-2014-4?IR=T&]

I'm sure many if us can relate to this diagram for it shows when most traders execute their trades. Of course there will be a small number of successful traders that had the mental (& financial) stretch to make use of such news-caused-fluctuation-effect.

Studying PBA's graph and also another, Datasonic Bhd would show a proper method for traders: Buying after a 'sudden decrease' in price. However so, note that such a method can prove unsuccessful if the company traded Stops giving out Exciting news.

Despite the above, it is seen that a purchase on a upward trend is most likely to give negative results if the trader fails to sell "in time". When is it time then? Well, there is no answer to this question but this remains the highest contributor to non successful trading and a cause of mental stress, sleep disorder and other anxiety related problems.

[Interestingly, insider trading is the best form for successful trading. However, it is illegal but note, with low conviction rate]

Datasonic is a great case study. An initial price of just above RM2 in May 2013, a high of RM10 at the end of 2013, share split, then an increase back to a high of RM4.87, then a sudden drop of 26% to RM3.58, a rise back to RM3.91 followed by a 27% drop to RM2.85. In short, the investor for the long term (May 2013-May 2014) would have reaped a gain of approximately 1200%. This company has one of the highest 1 year return stock. Despite the gains, if one observed the Trader's Graph, many would have fell into a disfavourable situation for investments made in 2014 (due to the warrants exercised and sale by those reaping their huge returns) until new Exciting news emerged yet again.

On an investment basis, it is least mentally taxing and financially beneficial to purchase stocks that have value; the means to continue successful operations at a low price that distributes profits generated to shareholders - the rightful owners of "Public" companies and recognises shareholders contribution (by not making unfavorable deals that would undermine shareholders). Businesses finance expansions via shareholders contribution thus it is only natural for the above suggestions.

This is rather a short post, for the Trader's Graph above summed up quite a lot.

Happy investing till next time.

Thursday, 10 April 2014

Market Outlook 2014

A question that has been ringing all year long, "Is THE Crash Coming?"

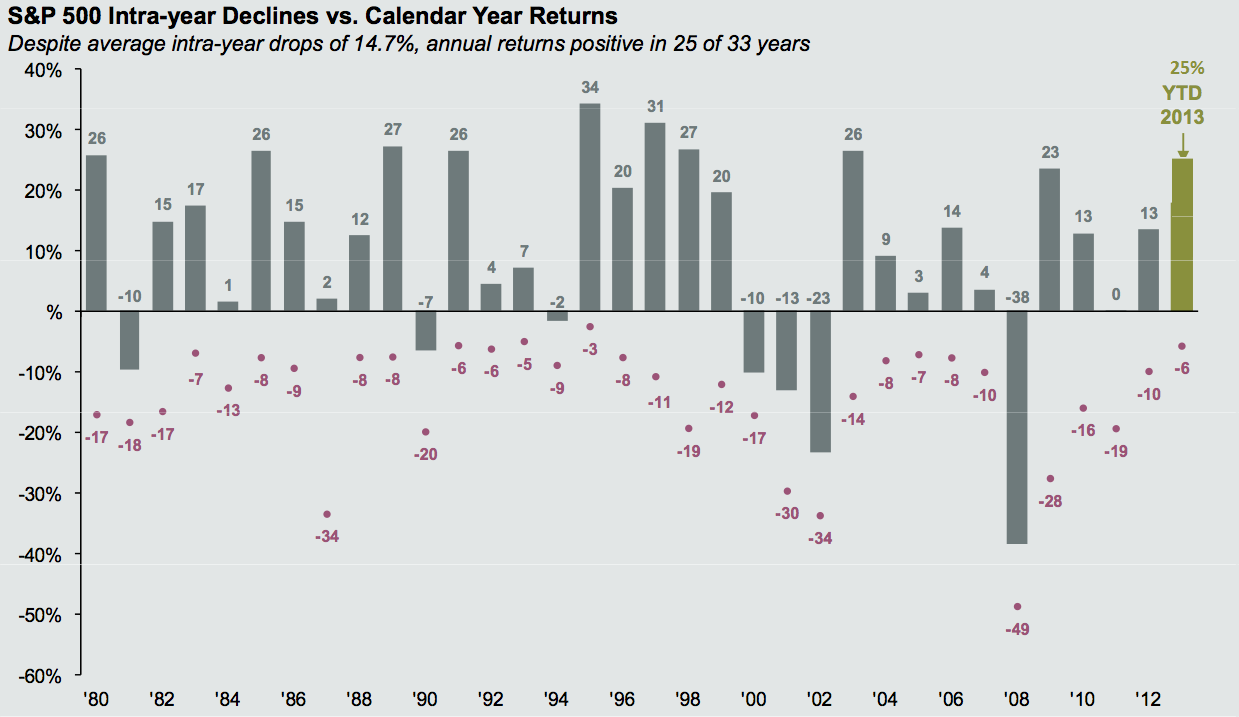

Have a look at the following link, which will show you the US market's Ups & Downs from 1980-2014.

(Corrections/additions for the graph: 2013-30% and 2014-1%)

Link: US Market - Ups & Downs 1980-2014

Why am I showing the above graph? This is because statistically now the following data can be concluded on:

How Frequently Corrections Occur on Average

- 5% market corrections : 3x per year

- 10% market corrections : 1x per year

- 20% market corrections : 1x every 3.5years

[Source: JP Morgan Fund - David Kelly]

This is because should you compare the KLCI graph against the S&P500, Dow Jones and NASDAQ(US indexes), you will find corresponding similarities (except the 1998 down)

Link: Comparison Graph by Yahoo Finance

Hence, the rife conclusion is that the Malaysian share market always tracks or follows the US market.

Despite the above statistics, the writer believes this SHOULD NOT be the case. Shares should be taken individually to a certain extent. How they perform should be based on how the company performs and it's continued performance in that particular economy.

[Note : Logic doesn't drive the market. A bear market MAY even push prices of well evaluated companies down]

In short, if you are holding great companies that should generate steady earnings and give you good dividends, perhaps any of the KLCI index companies, then you should only consider selling them if there are some major dynamic shifts in the company's fundamentals.

However, a question pops, why not sell and buy more when it gets lower (assuming a 2014 Market Doom)?

Before answering the above, let us view this. Theoretically, a "market doom" or "market crash" happens when major shareholders start selling off their holdings in big bulks. Some indications of such activity have been spotted since the 4th of April. According to CNBC, there was news of investors pulling out $400mil out of a $2+bil fund and hedge funds in the US selling off their stakes in momentum stocks.

These news make things more "scary" as tech stocks (usually termed momentum stocks) and stocks that have high valuations (high P/E ratio, no earnings but high prices) usually takes the first hit (drops) before a market downturn and which has been seen occurring recently in the US (since the 4th of April 2014).

These events occur as evaluations in US for many companies have long exceeded the acceptable limits suggested by Benjamin Graham amongst others, back in the 1930s when shares had P/Es of 10 or below. In today's world, the safe recommendation would be a P/E of below 20.

[Note : Creador, a private equity fund is of the view, valuations in Malaysia are still conservative. However, perhaps many companies have exceeded their valuations by the end of 2013 i.e. Oldtown hence the exit of the aforementioned fund of it's relatively substantial holding reaping huge returns)

P Price per share : What you pay

-- = ---------------------------

E Earnings per share : How much net profit a business makes per share that you own

Thus, when people realize that everyone realizes this over evaluations, a well grounded fear takes hold of the investors (you & others).

However so, back to the answer.

Good shares (big companies with good fundamentals). How long were you intending to hold your shares? If it is for the long term and you had bought your shares at a low price, then you should only sell knowing that these company will still perform, and that their prices may even increase as investors may now seek for these sort of companies. This is as no one can truly predict who is going to sell their major stake next driving prices down.

Shaky fundamentals stocks (bulls favourite)

Interestingly enough, momentum stocks do give good returns if traded properly or even as an investment if you were to have bought it earlier knowing the business background, it's affiliations & it's major shareholders. However, when you buy a stock that is not making any money or worse is losing money, do it knowing that one day this fact will come to light and start a bearish trend for your stock REGARDLESS of market outlook, for one major sell off by a substantial shareholder may unleash the bears. The saving grace would be that this stock may have a high liquidation value also known as current asset value, thus giving you a great return SHOULD the company dissolve. However, remember, businesses often strive to survive and may liquidate it's assets (rightfully-yours) or dilute per share value via rights offer (which indirectly forces shareholders to purchase more shares to prevent a drop in their shareholding value) to keep it afloat i.e. some airline company.

In a nutshell, the writer who has put aside some cash for investment (not much) would be more cautious in his purchases and only purchase shares that are fundamentally strong e.g. oligopolistics liquor companies, monopolistic companies, regaining popularity undervalued companies etc. The reason is that should there be a Market Correction not crash (as current over-valuations should be corrected), it would be much more beneficial to be greedy when others are fearful. Statistically, a few good purchases will outperform many mediocrely good purchases but one great purchase will of course triumph over all. Thus, a question unfolds. Are you willing to look for that one or diversify?

Until next time, keep your heads up, make wise decisions and happy investing.

Have a look at the following link, which will show you the US market's Ups & Downs from 1980-2014.

(Corrections/additions for the graph: 2013-30% and 2014-1%)

Link: US Market - Ups & Downs 1980-2014

{kind=link}

Why am I showing the above graph? This is because statistically now the following data can be concluded on:

How Frequently Corrections Occur on Average

- 5% market corrections : 3x per year

- 10% market corrections : 1x per year

- 20% market corrections : 1x every 3.5years

[Source: JP Morgan Fund - David Kelly]

This is because should you compare the KLCI graph against the S&P500, Dow Jones and NASDAQ(US indexes), you will find corresponding similarities (except the 1998 down)

Link: Comparison Graph by Yahoo Finance

Hence, the rife conclusion is that the Malaysian share market always tracks or follows the US market.

Despite the above statistics, the writer believes this SHOULD NOT be the case. Shares should be taken individually to a certain extent. How they perform should be based on how the company performs and it's continued performance in that particular economy.

[Note : Logic doesn't drive the market. A bear market MAY even push prices of well evaluated companies down]

In short, if you are holding great companies that should generate steady earnings and give you good dividends, perhaps any of the KLCI index companies, then you should only consider selling them if there are some major dynamic shifts in the company's fundamentals.

However, a question pops, why not sell and buy more when it gets lower (assuming a 2014 Market Doom)?

Before answering the above, let us view this. Theoretically, a "market doom" or "market crash" happens when major shareholders start selling off their holdings in big bulks. Some indications of such activity have been spotted since the 4th of April. According to CNBC, there was news of investors pulling out $400mil out of a $2+bil fund and hedge funds in the US selling off their stakes in momentum stocks.

These news make things more "scary" as tech stocks (usually termed momentum stocks) and stocks that have high valuations (high P/E ratio, no earnings but high prices) usually takes the first hit (drops) before a market downturn and which has been seen occurring recently in the US (since the 4th of April 2014).

These events occur as evaluations in US for many companies have long exceeded the acceptable limits suggested by Benjamin Graham amongst others, back in the 1930s when shares had P/Es of 10 or below. In today's world, the safe recommendation would be a P/E of below 20.

[Note : Creador, a private equity fund is of the view, valuations in Malaysia are still conservative. However, perhaps many companies have exceeded their valuations by the end of 2013 i.e. Oldtown hence the exit of the aforementioned fund of it's relatively substantial holding reaping huge returns)

P Price per share : What you pay

-- = ---------------------------

E Earnings per share : How much net profit a business makes per share that you own

Thus, when people realize that everyone realizes this over evaluations, a well grounded fear takes hold of the investors (you & others).

However so, back to the answer.

Good shares (big companies with good fundamentals). How long were you intending to hold your shares? If it is for the long term and you had bought your shares at a low price, then you should only sell knowing that these company will still perform, and that their prices may even increase as investors may now seek for these sort of companies. This is as no one can truly predict who is going to sell their major stake next driving prices down.

Shaky fundamentals stocks (bulls favourite)

Interestingly enough, momentum stocks do give good returns if traded properly or even as an investment if you were to have bought it earlier knowing the business background, it's affiliations & it's major shareholders. However, when you buy a stock that is not making any money or worse is losing money, do it knowing that one day this fact will come to light and start a bearish trend for your stock REGARDLESS of market outlook, for one major sell off by a substantial shareholder may unleash the bears. The saving grace would be that this stock may have a high liquidation value also known as current asset value, thus giving you a great return SHOULD the company dissolve. However, remember, businesses often strive to survive and may liquidate it's assets (rightfully-yours) or dilute per share value via rights offer (which indirectly forces shareholders to purchase more shares to prevent a drop in their shareholding value) to keep it afloat i.e. some airline company.

In a nutshell, the writer who has put aside some cash for investment (not much) would be more cautious in his purchases and only purchase shares that are fundamentally strong e.g. oligopolistics liquor companies, monopolistic companies, regaining popularity undervalued companies etc. The reason is that should there be a Market Correction not crash (as current over-valuations should be corrected), it would be much more beneficial to be greedy when others are fearful. Statistically, a few good purchases will outperform many mediocrely good purchases but one great purchase will of course triumph over all. Thus, a question unfolds. Are you willing to look for that one or diversify?

Until next time, keep your heads up, make wise decisions and happy investing.

Saturday, 5 April 2014

Understand Shares

Is the capital market is filled with inefficiencies? Inefficiencies in short, wrongly priced stocks. If your answer is yes, then by now you are willing to accept finding them would be rewarding.

And you would likely consider the numerous theories i.e. the efficient market hypothesis founded by esteem professors of prestigious institutions as fallacious or rather misleading.

So now, how do we find these stocks in Malaysia? First, we should understand some basics, i.e. the difference between the US market and the Malaysian market. The most compelling of them would be the number of shares in any given company. Take Parkson for example, having 1,012,000,000 shares as compared to the giant, Apple Inc with 891,990,000 shares (estimates by Bloomberg.com)

This would have great effect upon its price variation for it would logically require more shares to be purchased in a market to reach a higher price. Additionally there are 2 other forces working against price increments:

No. 1 The general idea of cheaper shares are more valuable &

No. 2 Our still young, large local fund dominated market with low foreign participation

Let's investigate No.1

A: 10000 shares of a RM0.50 issue

B: 2500 shares of a RM2.00 issue

(Note that interestingly enough, your initial investment in both companies would be the same for the given examples, which is RM5000.00.)

Is company A a better investment than company B?

If your answer is yes, then you are right, ASSUMING both companies prices rise by RM0.05. But why? Because company A is cheaper?

NO.

This is because an increase of RM0.05 in company A would mean a 10% increase in value whereas only a mediocre 2.5% increase in company B.