Trading is speculation whereby you buy and sell stocks for short term gains. Speculation is when you buy something without solid justified reasons.

For example, PBA Bhd shares as of late suddenly had a surge in price upon news of high chances of a rate hike. The higher share price now can only be justified as an "investment" if;

1) the rate hike is executed

2) the current price does not yet reflect an increase profits to be realized

3) etc.

PBA graph:

[http://www.bursamalaysia.com/market/listed-companies/list-of-companies/plc-profile.html?stock_code=5041]

However, a bursa Malaysia graph of PBA would show a price movement from RM1.16 to RM1.65, beginning of April to its peak towards the end of the month. That is a 42% increase. Could the new rates YET to be implemented have a 42% increase in profits (assuming the company is worth RM1.16 as of end of March 2014) ? And if the answer is yes, will the profit be distributed to the shareholders via dividends amongst other ways?

A simple solution, have a look at this digram (nicknamed Trader's Graph)

[http://www.businessinsider.com/how-not-to-invest-2014-4?IR=T&]

I'm sure many if us can relate to this diagram for it shows when most traders execute their trades. Of course there will be a small number of successful traders that had the mental (& financial) stretch to make use of such news-caused-fluctuation-effect.

Studying PBA's graph and also another, Datasonic Bhd would show a proper method for traders: Buying after a 'sudden decrease' in price. However so, note that such a method can prove unsuccessful if the company traded Stops giving out Exciting news.

Despite the above, it is seen that a purchase on a upward trend is most likely to give negative results if the trader fails to sell "in time". When is it time then? Well, there is no answer to this question but this remains the highest contributor to non successful trading and a cause of mental stress, sleep disorder and other anxiety related problems.

[Interestingly, insider trading is the best form for successful trading. However, it is illegal but note, with low conviction rate]

Datasonic is a great case study. An initial price of just above RM2 in May 2013, a high of RM10 at the end of 2013, share split, then an increase back to a high of RM4.87, then a sudden drop of 26% to RM3.58, a rise back to RM3.91 followed by a 27% drop to RM2.85. In short, the investor for the long term (May 2013-May 2014) would have reaped a gain of approximately 1200%. This company has one of the highest 1 year return stock. Despite the gains, if one observed the Trader's Graph, many would have fell into a disfavourable situation for investments made in 2014 (due to the warrants exercised and sale by those reaping their huge returns) until new Exciting news emerged yet again.

On an investment basis, it is least mentally taxing and financially beneficial to purchase stocks that have value; the means to continue successful operations at a low price that distributes profits generated to shareholders - the rightful owners of "Public" companies and recognises shareholders contribution (by not making unfavorable deals that would undermine shareholders). Businesses finance expansions via shareholders contribution thus it is only natural for the above suggestions.

This is rather a short post, for the Trader's Graph above summed up quite a lot.

Happy investing till next time.

Sunday, 27 April 2014

Thursday, 10 April 2014

Market Outlook 2014

A question that has been ringing all year long, "Is THE Crash Coming?"

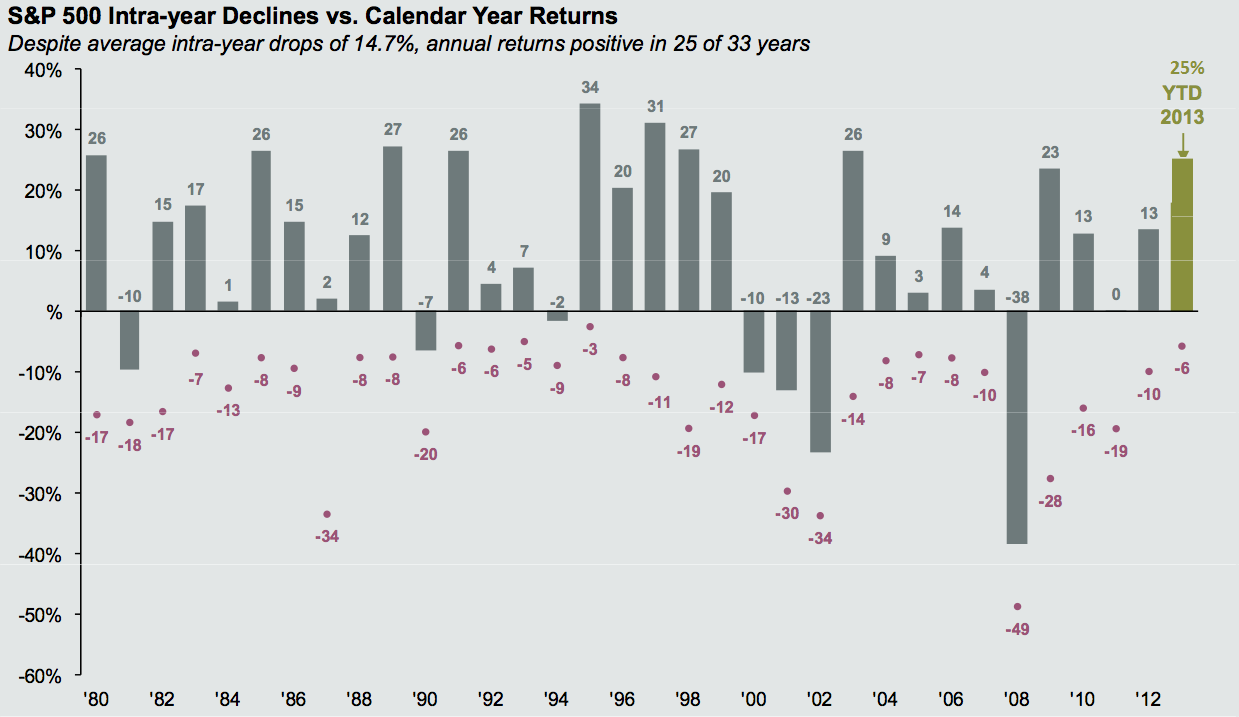

Have a look at the following link, which will show you the US market's Ups & Downs from 1980-2014.

(Corrections/additions for the graph: 2013-30% and 2014-1%)

Link: US Market - Ups & Downs 1980-2014

Why am I showing the above graph? This is because statistically now the following data can be concluded on:

How Frequently Corrections Occur on Average

- 5% market corrections : 3x per year

- 10% market corrections : 1x per year

- 20% market corrections : 1x every 3.5years

[Source: JP Morgan Fund - David Kelly]

This is because should you compare the KLCI graph against the S&P500, Dow Jones and NASDAQ(US indexes), you will find corresponding similarities (except the 1998 down)

Link: Comparison Graph by Yahoo Finance

Hence, the rife conclusion is that the Malaysian share market always tracks or follows the US market.

Despite the above statistics, the writer believes this SHOULD NOT be the case. Shares should be taken individually to a certain extent. How they perform should be based on how the company performs and it's continued performance in that particular economy.

[Note : Logic doesn't drive the market. A bear market MAY even push prices of well evaluated companies down]

In short, if you are holding great companies that should generate steady earnings and give you good dividends, perhaps any of the KLCI index companies, then you should only consider selling them if there are some major dynamic shifts in the company's fundamentals.

However, a question pops, why not sell and buy more when it gets lower (assuming a 2014 Market Doom)?

Before answering the above, let us view this. Theoretically, a "market doom" or "market crash" happens when major shareholders start selling off their holdings in big bulks. Some indications of such activity have been spotted since the 4th of April. According to CNBC, there was news of investors pulling out $400mil out of a $2+bil fund and hedge funds in the US selling off their stakes in momentum stocks.

These news make things more "scary" as tech stocks (usually termed momentum stocks) and stocks that have high valuations (high P/E ratio, no earnings but high prices) usually takes the first hit (drops) before a market downturn and which has been seen occurring recently in the US (since the 4th of April 2014).

These events occur as evaluations in US for many companies have long exceeded the acceptable limits suggested by Benjamin Graham amongst others, back in the 1930s when shares had P/Es of 10 or below. In today's world, the safe recommendation would be a P/E of below 20.

[Note : Creador, a private equity fund is of the view, valuations in Malaysia are still conservative. However, perhaps many companies have exceeded their valuations by the end of 2013 i.e. Oldtown hence the exit of the aforementioned fund of it's relatively substantial holding reaping huge returns)

P Price per share : What you pay

-- = ---------------------------

E Earnings per share : How much net profit a business makes per share that you own

Thus, when people realize that everyone realizes this over evaluations, a well grounded fear takes hold of the investors (you & others).

However so, back to the answer.

Good shares (big companies with good fundamentals). How long were you intending to hold your shares? If it is for the long term and you had bought your shares at a low price, then you should only sell knowing that these company will still perform, and that their prices may even increase as investors may now seek for these sort of companies. This is as no one can truly predict who is going to sell their major stake next driving prices down.

Shaky fundamentals stocks (bulls favourite)

Interestingly enough, momentum stocks do give good returns if traded properly or even as an investment if you were to have bought it earlier knowing the business background, it's affiliations & it's major shareholders. However, when you buy a stock that is not making any money or worse is losing money, do it knowing that one day this fact will come to light and start a bearish trend for your stock REGARDLESS of market outlook, for one major sell off by a substantial shareholder may unleash the bears. The saving grace would be that this stock may have a high liquidation value also known as current asset value, thus giving you a great return SHOULD the company dissolve. However, remember, businesses often strive to survive and may liquidate it's assets (rightfully-yours) or dilute per share value via rights offer (which indirectly forces shareholders to purchase more shares to prevent a drop in their shareholding value) to keep it afloat i.e. some airline company.

In a nutshell, the writer who has put aside some cash for investment (not much) would be more cautious in his purchases and only purchase shares that are fundamentally strong e.g. oligopolistics liquor companies, monopolistic companies, regaining popularity undervalued companies etc. The reason is that should there be a Market Correction not crash (as current over-valuations should be corrected), it would be much more beneficial to be greedy when others are fearful. Statistically, a few good purchases will outperform many mediocrely good purchases but one great purchase will of course triumph over all. Thus, a question unfolds. Are you willing to look for that one or diversify?

Until next time, keep your heads up, make wise decisions and happy investing.

Have a look at the following link, which will show you the US market's Ups & Downs from 1980-2014.

(Corrections/additions for the graph: 2013-30% and 2014-1%)

Link: US Market - Ups & Downs 1980-2014

{kind=link}

Why am I showing the above graph? This is because statistically now the following data can be concluded on:

How Frequently Corrections Occur on Average

- 5% market corrections : 3x per year

- 10% market corrections : 1x per year

- 20% market corrections : 1x every 3.5years

[Source: JP Morgan Fund - David Kelly]

This is because should you compare the KLCI graph against the S&P500, Dow Jones and NASDAQ(US indexes), you will find corresponding similarities (except the 1998 down)

Link: Comparison Graph by Yahoo Finance

Hence, the rife conclusion is that the Malaysian share market always tracks or follows the US market.

Despite the above statistics, the writer believes this SHOULD NOT be the case. Shares should be taken individually to a certain extent. How they perform should be based on how the company performs and it's continued performance in that particular economy.

[Note : Logic doesn't drive the market. A bear market MAY even push prices of well evaluated companies down]

In short, if you are holding great companies that should generate steady earnings and give you good dividends, perhaps any of the KLCI index companies, then you should only consider selling them if there are some major dynamic shifts in the company's fundamentals.

However, a question pops, why not sell and buy more when it gets lower (assuming a 2014 Market Doom)?

Before answering the above, let us view this. Theoretically, a "market doom" or "market crash" happens when major shareholders start selling off their holdings in big bulks. Some indications of such activity have been spotted since the 4th of April. According to CNBC, there was news of investors pulling out $400mil out of a $2+bil fund and hedge funds in the US selling off their stakes in momentum stocks.

These news make things more "scary" as tech stocks (usually termed momentum stocks) and stocks that have high valuations (high P/E ratio, no earnings but high prices) usually takes the first hit (drops) before a market downturn and which has been seen occurring recently in the US (since the 4th of April 2014).

These events occur as evaluations in US for many companies have long exceeded the acceptable limits suggested by Benjamin Graham amongst others, back in the 1930s when shares had P/Es of 10 or below. In today's world, the safe recommendation would be a P/E of below 20.

[Note : Creador, a private equity fund is of the view, valuations in Malaysia are still conservative. However, perhaps many companies have exceeded their valuations by the end of 2013 i.e. Oldtown hence the exit of the aforementioned fund of it's relatively substantial holding reaping huge returns)

P Price per share : What you pay

-- = ---------------------------

E Earnings per share : How much net profit a business makes per share that you own

Thus, when people realize that everyone realizes this over evaluations, a well grounded fear takes hold of the investors (you & others).

However so, back to the answer.

Good shares (big companies with good fundamentals). How long were you intending to hold your shares? If it is for the long term and you had bought your shares at a low price, then you should only sell knowing that these company will still perform, and that their prices may even increase as investors may now seek for these sort of companies. This is as no one can truly predict who is going to sell their major stake next driving prices down.

Shaky fundamentals stocks (bulls favourite)

Interestingly enough, momentum stocks do give good returns if traded properly or even as an investment if you were to have bought it earlier knowing the business background, it's affiliations & it's major shareholders. However, when you buy a stock that is not making any money or worse is losing money, do it knowing that one day this fact will come to light and start a bearish trend for your stock REGARDLESS of market outlook, for one major sell off by a substantial shareholder may unleash the bears. The saving grace would be that this stock may have a high liquidation value also known as current asset value, thus giving you a great return SHOULD the company dissolve. However, remember, businesses often strive to survive and may liquidate it's assets (rightfully-yours) or dilute per share value via rights offer (which indirectly forces shareholders to purchase more shares to prevent a drop in their shareholding value) to keep it afloat i.e. some airline company.

In a nutshell, the writer who has put aside some cash for investment (not much) would be more cautious in his purchases and only purchase shares that are fundamentally strong e.g. oligopolistics liquor companies, monopolistic companies, regaining popularity undervalued companies etc. The reason is that should there be a Market Correction not crash (as current over-valuations should be corrected), it would be much more beneficial to be greedy when others are fearful. Statistically, a few good purchases will outperform many mediocrely good purchases but one great purchase will of course triumph over all. Thus, a question unfolds. Are you willing to look for that one or diversify?

Until next time, keep your heads up, make wise decisions and happy investing.

Saturday, 5 April 2014

Understand Shares

Is the capital market is filled with inefficiencies? Inefficiencies in short, wrongly priced stocks. If your answer is yes, then by now you are willing to accept finding them would be rewarding.

And you would likely consider the numerous theories i.e. the efficient market hypothesis founded by esteem professors of prestigious institutions as fallacious or rather misleading.

So now, how do we find these stocks in Malaysia? First, we should understand some basics, i.e. the difference between the US market and the Malaysian market. The most compelling of them would be the number of shares in any given company. Take Parkson for example, having 1,012,000,000 shares as compared to the giant, Apple Inc with 891,990,000 shares (estimates by Bloomberg.com)

This would have great effect upon its price variation for it would logically require more shares to be purchased in a market to reach a higher price. Additionally there are 2 other forces working against price increments:

No. 1 The general idea of cheaper shares are more valuable &

No. 2 Our still young, large local fund dominated market with low foreign participation

Let's investigate No.1

A: 10000 shares of a RM0.50 issue

B: 2500 shares of a RM2.00 issue

(Note that interestingly enough, your initial investment in both companies would be the same for the given examples, which is RM5000.00.)

Is company A a better investment than company B?

If your answer is yes, then you are right, ASSUMING both companies prices rise by RM0.05. But why? Because company A is cheaper?

NO.

This is because an increase of RM0.05 in company A would mean a 10% increase in value whereas only a mediocre 2.5% increase in company B.

Now that we understand the above we could relatively conclude the lower the price of an issue, the greater it appreciates comparing to a more expensive issue assuming the same increment in price (RM0.05) hence a better investment.

The above is only true if the above scenario occurs. More likely than not, the cheaper stocks fluctuate less than the more expensive stocks as the overall market value of the latter are usually higher.

Take Hubline and Aeon as examples. These are two companies of high number of shares. An investment of RM5000 in Hubline Bhd previously when the market price was RM0.05 and a sale at RM0.055 would have given you a 10% return: RM500. An investment in Aeon Bhd during the latter period(RM12) when the market price fell from RM18 to RM12 would have given you a return of RM833.33 assuming you sold when it appreciated to RM14.00 (current price RM15.24).

Do you think it was wiser to have invested in Hubline a still negative earnings registering company or in Aeon a profit making company that suffered a over-price decrease due to overheated fear of slowing of the retail industry?

There are no wrong answers here as long as your investment appreciates. But the reality is that purchasing Aeon would have been better because you would have owned partly of a great business that had better financial ratios, better earnings and consequently better value.

Hence a conclusion to be drawn is that the price of a company should not deter your investment decisions. However, if you are a trader, you may ignore this statement for short positions taken, smaller appreciation in cheaper issues will always do better but do it upon recognizing the higher risk to be undertaken in terms of value purchasing. Remember, price appreciation doesn't make your decision right and a precise depreciation doesn't make you wrong either. It would just mean you somehow made a conclusion to the issue's prospect and took a profit/loss based on that conclusion.

Coming to No. 2.

Malaysian market has still to undergo many more development in its financial products i.e. options, warrants, swaps, mortgage, open end short selling, etc, and especially the opening up to foreign holdings. Currently EPF and other such mega funds dominate the market for prices of companies move in tandem with their holdings. In short, knowing what EPF is buying/selling may likely benefit your investments more often than not.

However, this may be tiresome for some, to keep up with mega funds purchases, business developments, political affairs, US market, speculative sentiments via Theedge newspaper-like news, gossips, etc.

The safest bet in the writers opinion is to find a good company that usually has public appeal but is now approaching the end of a down cycle. Of course this company should have good financials and management amongst others.

As for now, knowing these basics should help you investors and traders alike in understanding the relative nature of the Malaysian market. Feel free to comment for the writer believes in the continual accumulation of knowledge. In Warren Buffett's words, the best investment you can make is an investment in yourself. Until next time, happy investing.

And you would likely consider the numerous theories i.e. the efficient market hypothesis founded by esteem professors of prestigious institutions as fallacious or rather misleading.

So now, how do we find these stocks in Malaysia? First, we should understand some basics, i.e. the difference between the US market and the Malaysian market. The most compelling of them would be the number of shares in any given company. Take Parkson for example, having 1,012,000,000 shares as compared to the giant, Apple Inc with 891,990,000 shares (estimates by Bloomberg.com)

This would have great effect upon its price variation for it would logically require more shares to be purchased in a market to reach a higher price. Additionally there are 2 other forces working against price increments:

No. 1 The general idea of cheaper shares are more valuable &

No. 2 Our still young, large local fund dominated market with low foreign participation

Let's investigate No.1

A: 10000 shares of a RM0.50 issue

B: 2500 shares of a RM2.00 issue

(Note that interestingly enough, your initial investment in both companies would be the same for the given examples, which is RM5000.00.)

Is company A a better investment than company B?

If your answer is yes, then you are right, ASSUMING both companies prices rise by RM0.05. But why? Because company A is cheaper?

NO.

This is because an increase of RM0.05 in company A would mean a 10% increase in value whereas only a mediocre 2.5% increase in company B.

Now that we understand the above we could relatively conclude the lower the price of an issue, the greater it appreciates comparing to a more expensive issue assuming the same increment in price (RM0.05) hence a better investment.

The above is only true if the above scenario occurs. More likely than not, the cheaper stocks fluctuate less than the more expensive stocks as the overall market value of the latter are usually higher.

Take Hubline and Aeon as examples. These are two companies of high number of shares. An investment of RM5000 in Hubline Bhd previously when the market price was RM0.05 and a sale at RM0.055 would have given you a 10% return: RM500. An investment in Aeon Bhd during the latter period(RM12) when the market price fell from RM18 to RM12 would have given you a return of RM833.33 assuming you sold when it appreciated to RM14.00 (current price RM15.24).

Do you think it was wiser to have invested in Hubline a still negative earnings registering company or in Aeon a profit making company that suffered a over-price decrease due to overheated fear of slowing of the retail industry?

There are no wrong answers here as long as your investment appreciates. But the reality is that purchasing Aeon would have been better because you would have owned partly of a great business that had better financial ratios, better earnings and consequently better value.

Hence a conclusion to be drawn is that the price of a company should not deter your investment decisions. However, if you are a trader, you may ignore this statement for short positions taken, smaller appreciation in cheaper issues will always do better but do it upon recognizing the higher risk to be undertaken in terms of value purchasing. Remember, price appreciation doesn't make your decision right and a precise depreciation doesn't make you wrong either. It would just mean you somehow made a conclusion to the issue's prospect and took a profit/loss based on that conclusion.

Coming to No. 2.

Malaysian market has still to undergo many more development in its financial products i.e. options, warrants, swaps, mortgage, open end short selling, etc, and especially the opening up to foreign holdings. Currently EPF and other such mega funds dominate the market for prices of companies move in tandem with their holdings. In short, knowing what EPF is buying/selling may likely benefit your investments more often than not.

However, this may be tiresome for some, to keep up with mega funds purchases, business developments, political affairs, US market, speculative sentiments via Theedge newspaper-like news, gossips, etc.

The safest bet in the writers opinion is to find a good company that usually has public appeal but is now approaching the end of a down cycle. Of course this company should have good financials and management amongst others.

As for now, knowing these basics should help you investors and traders alike in understanding the relative nature of the Malaysian market. Feel free to comment for the writer believes in the continual accumulation of knowledge. In Warren Buffett's words, the best investment you can make is an investment in yourself. Until next time, happy investing.

Subscribe to:

Posts (Atom)